The price of Hinkley, the value of Hinkley

Why £133/MWh is the wrong number to argue about — and what Flamanville's first 16 months reveal

To many, nuclear is the cavalry that will save the grid, net zero and our industrial competitiveness. Stable, reliable, baseload power using a technology independent of current weather conditions, deployed at scale for 75 years.

When the final investment decision for Hinkley Point C was made, the plan was to commission in 2025. That slipped to the current hope to launch one of the two 1.6GW units in 2030, with another unit to follow one or two years later.

However, if we’re to hope that it will synchronise and immediately output 1.6GW, one should take a cautionary look at the performance of EDF’s sister project in Flamanville (Normandy), which after many years of delays commissioned in 2025.

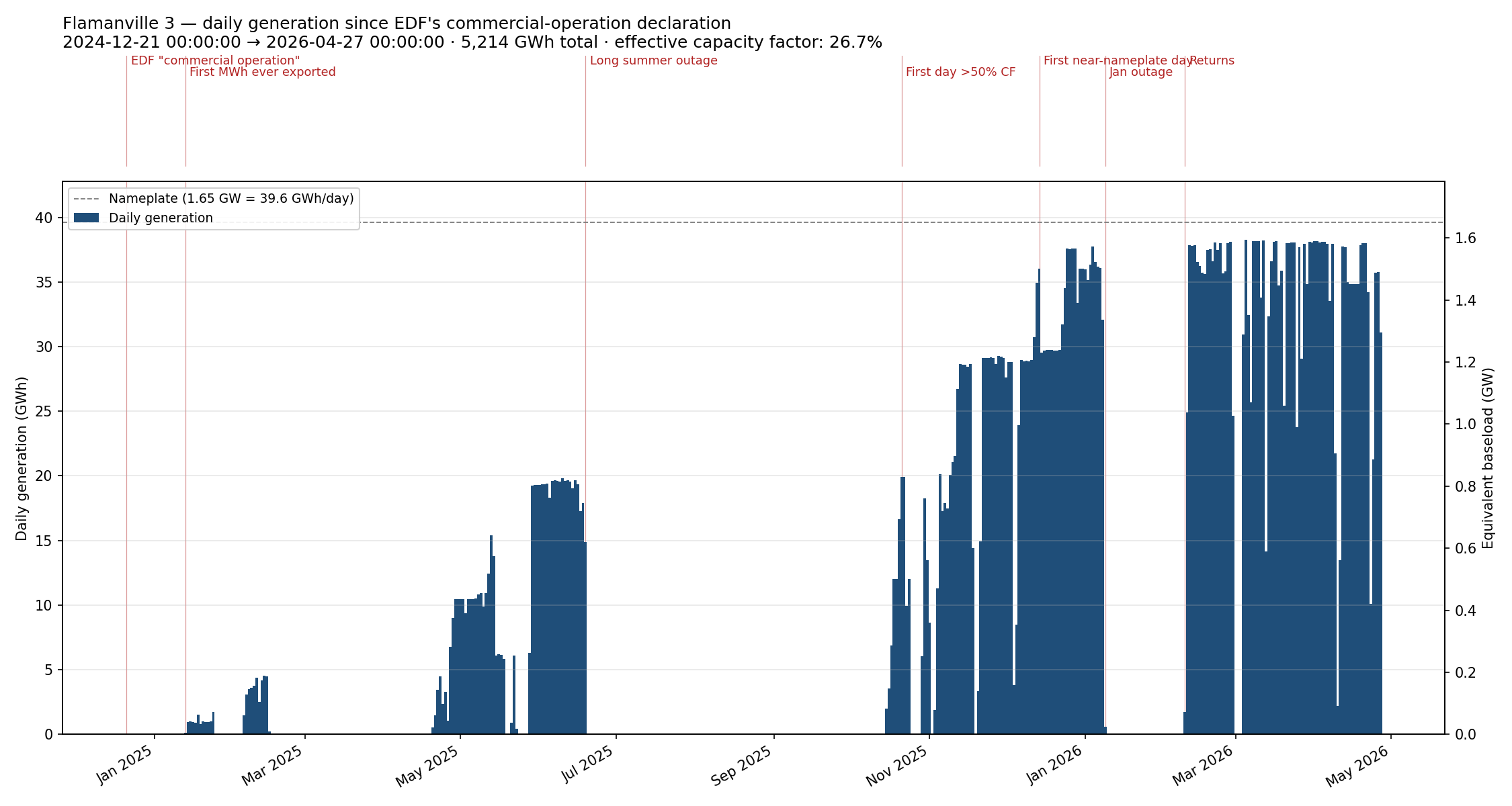

It really hasn’t been plain-sailing. In the sixteen months since EDF formally declared commercial operation in late December 2024, Flamanville 3 has been offline for 285 of those days — an availability of around 42 per cent and an effective capacity factor of 27 per cent, about half that of our best wind farms. The design figure for an EPR nuclear reactor is closer to 90.

The damage comes from three big stoppages and a long list of small ones. The first ran for 65 days through February to April 2025. It started with a sensor reading on one of the cooling systems, gathered some turbine-bearing maintenance along the way, and ended up needing “additional work” deeper in the nuclear island — the classic while-we’re-in-here pattern. The second was longer still, running 117 days through the summer, to hand-polish — yes, hand-polish — three safety valves on the primary circuit; irregularities had been found on two and EDF pulled the third out as well, just to be sure. The third, 32 days in January and February of this year, wasn’t really a Flamanville problem at all. Storm Goretti made landfall in Normandy and EDF tripped the reactor offline as a precaution. The unit didn’t return until 9 February. Imagine a wind farm doing the same?

What’s striking is that the reactor itself has only tripped automatically once in those sixteen months. The lost output has come from auxiliary equipment, commissioning slippage, and one piece of weather. The nuclear bit is, by and large, behaving. It’s everything around it that isn’t.

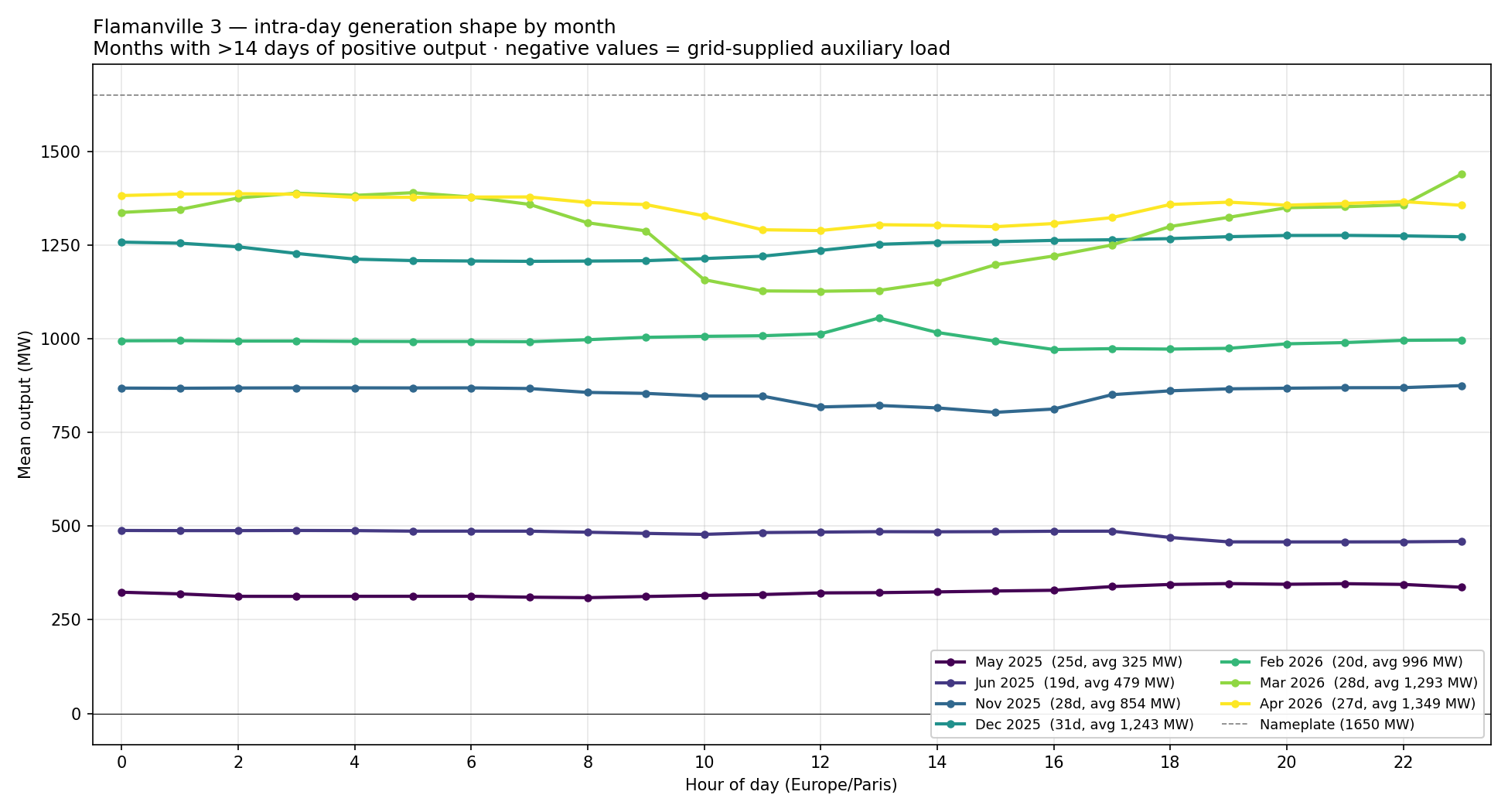

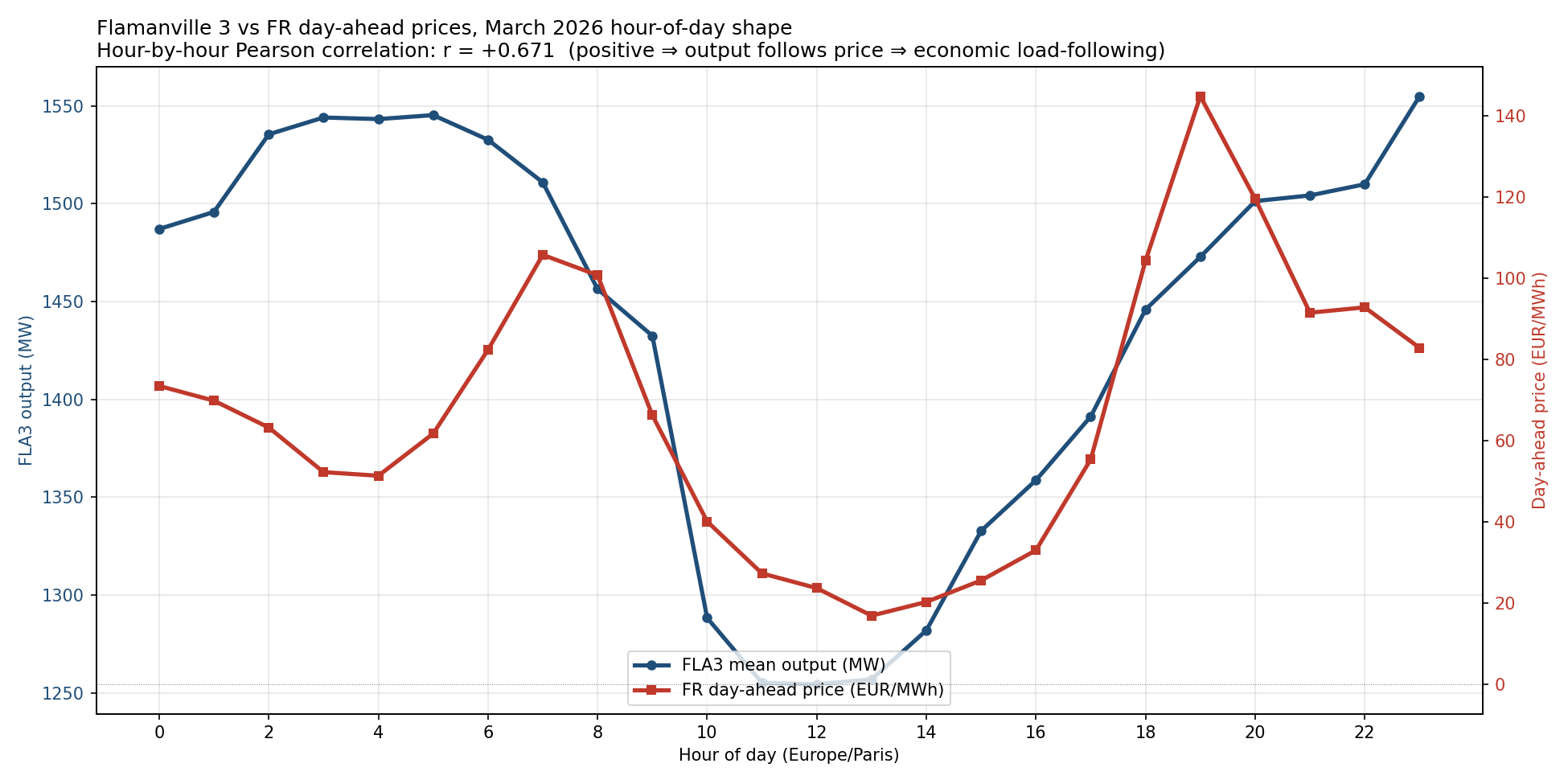

Another innovation in France limiting output is the flexing of nuclear output downward in the middle of the day. To my knowledge, this has never been a requirement of the existing British nuclear fleet, and won’t be possible at Hinkley Point C. Traditionally, flexing output at nuclear plant has been known to increase wear and tear; so it’s notable at Flamanville, just a year into its commercial operation1 Watch this space for a deeper dive into nuclear flexibility.

Now for a thought experiment. Let’s imagine that, instead of commissioning last February in the UK, that the Flamanville reactor was the first reactor to be commissioned at Hinkley Point. It’s also being built by EDF and shares some (but not all) of its design. So I feel the comparison is not unrealistic.

On the one hand, Hinkley’s arrival just before the Iran war might have felt like a blessing, especially on Britain’s grid that it much more exposed to gas power. Certainly, this would be true for energy security. But in terms of cost, the situation is different.

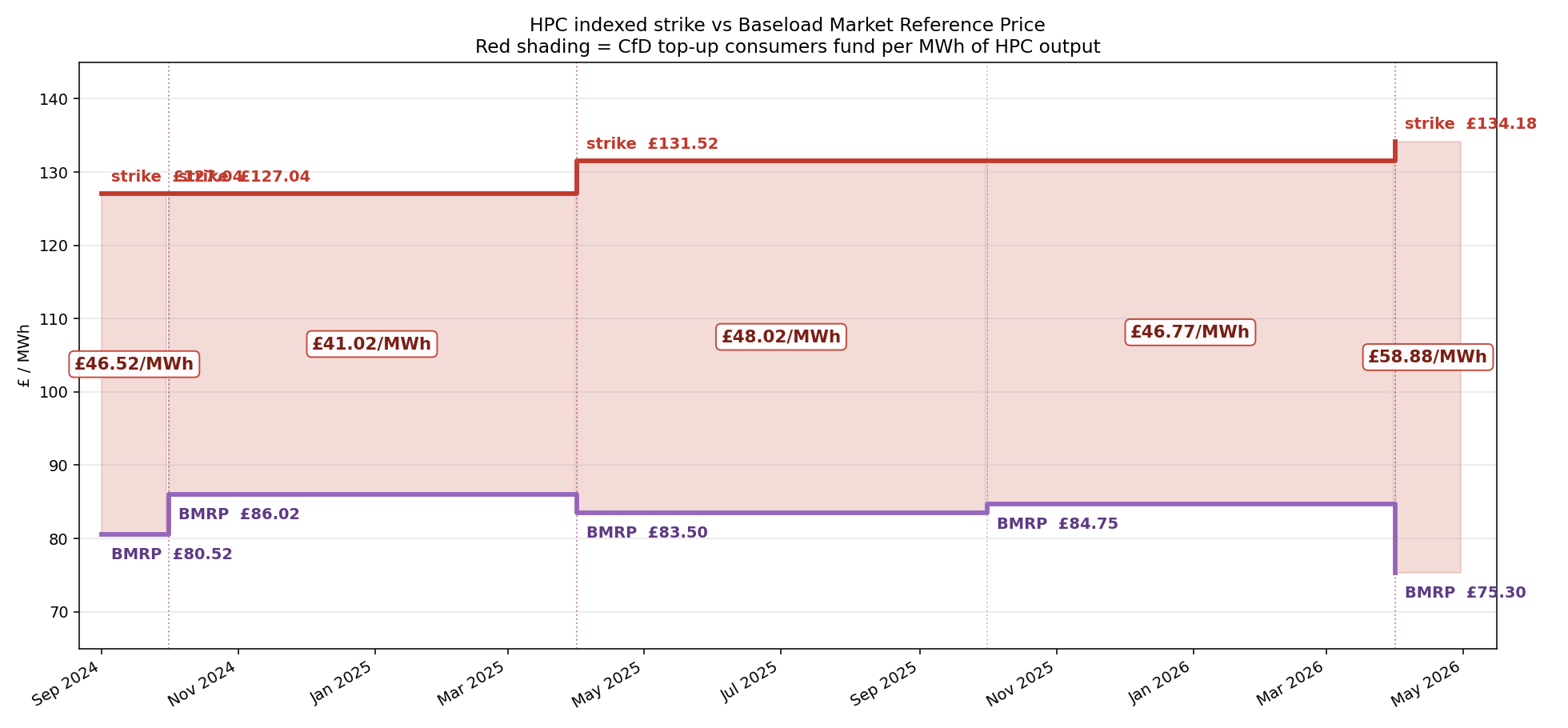

The Strike Price for Hinkley Point C has increased substantially since the contract was signed in 2016. Even after a 3% discount was applied for economies of scale after Government gave the go ahead to Sizewell C, after years of inflation it stands at £133/MWh for the year starting in April 2026.

So, if Hinkley (Flamanville 3) had been generating for the British grid over the last year, consumers would have paid a top-up of about £248m, or £48/MWh for each unit it generated in order to make up EDF’s revenues to the level allowed by the strike price. Now I haven’t re-run a grid model to fully simulate the impact on wholesale prices, but Hinkley’s presence would reduce them, so I feel confident to say the subsidy figure is a lower bound.

Interestingly as well, because the CfD reference price for Hinkley is the baseload market reference. used for biomass plant, rather than the day ahead market reference price more widely known for wind farms, and because this has been less volatile in response to the Iran conflict (it operates with more of a lag as it more forward lookng), the top-up wouldn’t yet have been clawed back for consumers.

So would an early commissioning of Hinkley have been unambiguously bad for consumers? In fact, the CfD isn’t the complete picture for a couple of reasons. As its fashionable to now say, the Levelised Cost of Energy is not a comprehensive measure of system or consumer costs.