Did the price-cap kill household energy competition?

Or is Octopus simply too good? What might happen next to the price cap?

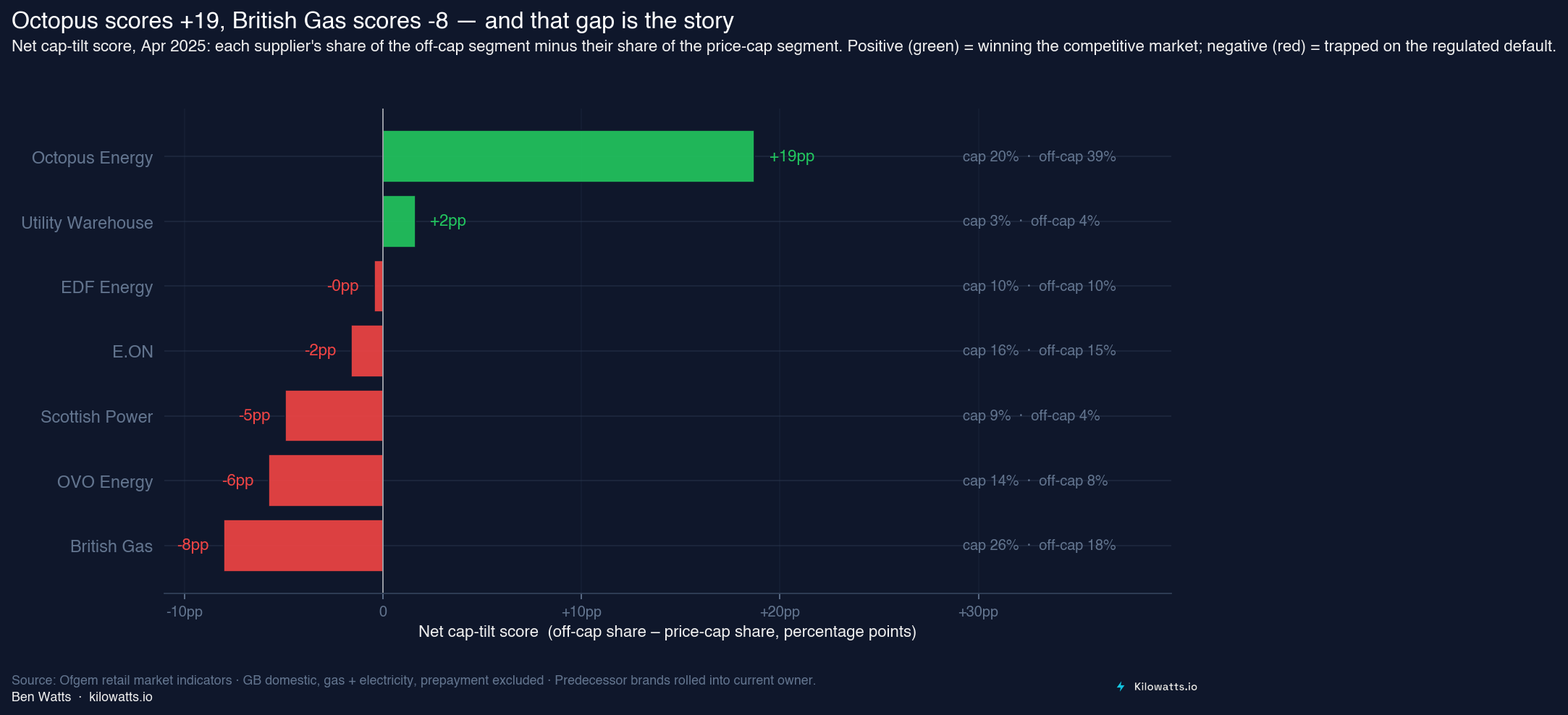

I recently used Ofgem data to create a net approval score for household energy, where suppliers are compared on their ability to win the trust of consumers and move off the Ofgem pricecap:

Four moments that summarise it:

2013, Ed Miliband campaigns on capping energy prices (Octopus doesn’t yet exist - except as a twinkle in Greg Jackson’s eye).

2018, after nearly “loosing” the 2017 election, Theresa May’s government legislates the cap (Octopus has under 1% of the market).

2022–23, the Treasury spends £46bn through suppliers to subsidise the cap through the wholesale crisis rather than reform it (Octopus takes over Bulb and gains momentum).

2025, the chart above. The cap preoccupied and muted Octopus’s competitors into complacency; Octopus itself rose despite it, indeed perhaps because of it.

The line between those four moments, Octopus’ rise that ran alongside, plus three plausible reforms the price cap are the back half of this piece. Spoiler, the most uncomfortable of those is the one we’ll probably end up taking.